Does Homeowners Insurance Cover Rotting Wood? Know The Facts

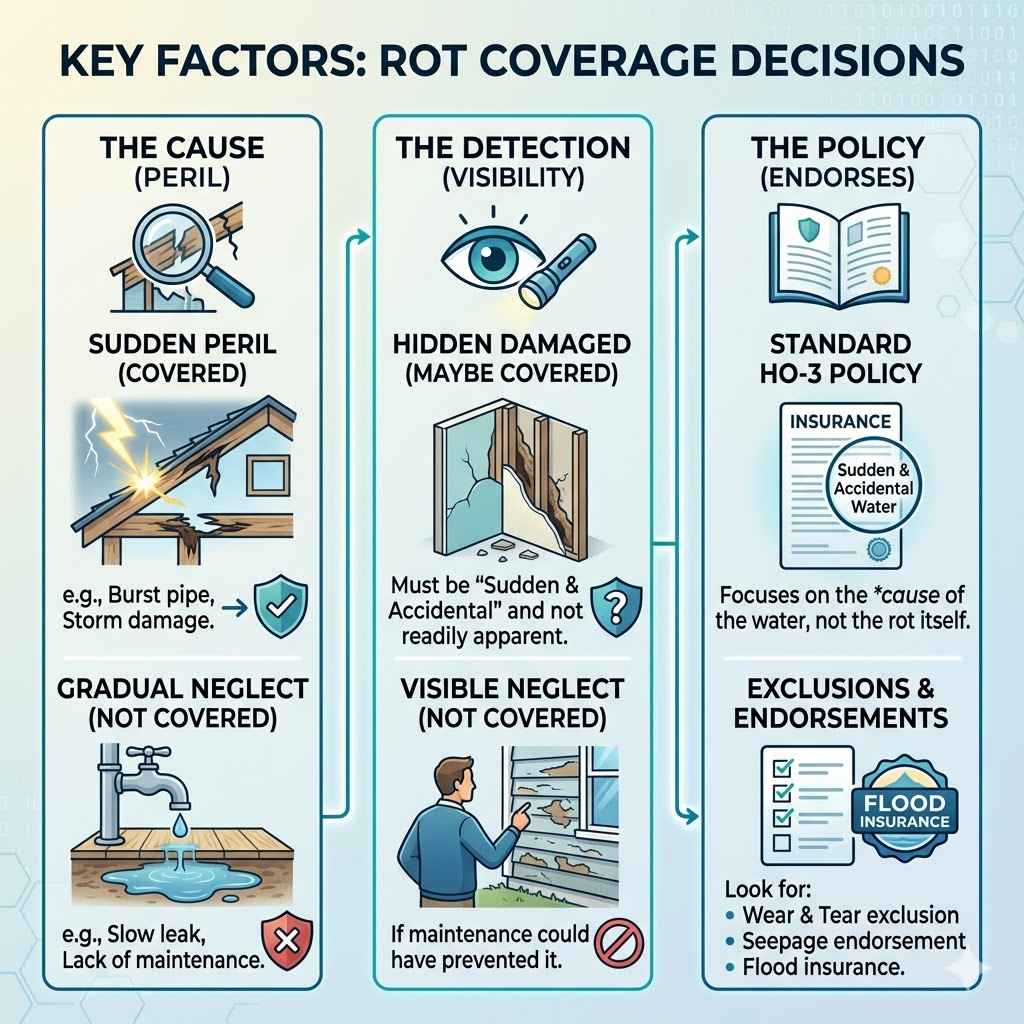

Homeowners insurance is there to protect you from unexpected damage. But it has limits. Policies are designed to cover sudden and accidental events.

Think of a burst pipe that causes water damage. That’s usually covered. Rotting wood often develops over a long time.

This slow development is key. Insurance companies look at how the damage occurred. Was it a sudden event?

Or did it happen slowly due to neglect or poor maintenance? This difference matters a lot for your claim.

Most standard policies, like the HO-3 form common in the U.S., cover “sudden and accidental” damage. They also list specific perils that are covered. Things like fire, windstorms, and vandalism are often on this list.

But they also have a list of exclusions. These are things your insurance will NOT cover.

Rot is rarely listed as a covered peril. Instead, it’s often an exclusion or a result of an excluded peril. This means if rot is found, your claim might be denied.

It depends on the root cause of the rot. That’s the most important part to figure out. Your policy will often cover damage resulting from a covered peril.

But it might not cover the rot itself.

For example, if a heavy rainstorm causes a roof leak (a sudden event), and that leak leads to wood rot over a few months, your insurance might cover the resulting rot damage. This is because the initial cause was a covered peril. But if the roof has been leaking for years due to poor maintenance, and rot sets in, the insurance company will likely deny the claim.

It’s crucial to read your policy documents. Look for sections on “water damage,” “mold,” and “wear and tear.” These sections often explain how rot is treated. Sometimes, specific endorsements or riders can add coverage for certain types of water damage that might lead to rot.

But these are less common for general rot issues.

The expertise of your insurance adjuster is also vital. They will investigate the cause. They look for evidence of how long the damage has been present.

This includes inspecting the affected areas. They might also review repair history or maintenance records. Proving a sudden cause can be your best bet for coverage.

But often, rot is a slow creep.

Understanding these nuances is the first step. It helps you know what to expect. It also guides you on what actions to take.

Acting quickly is always best. Don’t wait for the problem to get worse. This can make coverage even more unlikely.

It also leads to more expensive repairs.

My Own Homeowner’s Nightmare: The Rotting Deck Saga

I remember one sweltering summer day, about five years ago. I was planning a backyard BBQ. I decided to give the old wooden deck a good scrub.

As I was sweeping, my broom just… fell through a section of the decking. It wasn’t a small hole; it was like the wood had turned to soft, damp sponge. Panic set in instantly.

I knelt down, feeling the wood. It was crumbly and wet. I could see dark, blackish patches and a faint, unpleasant musty smell.

My mind raced. “This can’t be good. This is going to cost a fortune!” I immediately thought about my homeowners insurance.

Surely, they would cover something like this? My deck was only about 10 years old.

I called my insurance agent that same afternoon. I explained the situation, trying to sound calm. My deck board just broke, and the wood is all rotten,” I said.

The agent listened patiently. Then came the familiar, dreaded questions. “Has it been raining a lot lately?

Have you noticed any leaks near the deck? When did you last seal or treat the deck?”

These questions made me pause. The truth was, I hadn’t sealed the deck in maybe three years. Life got busy.

And yes, we’d had a particularly wet spring. There had been a few small puddles that didn’t drain quite right near that corner of the deck. It wasn’t a sudden flood or a storm damage event.

The agent explained that most policies cover sudden, accidental damage. Rot, she explained, is usually a gradual thing. It happens over time due to moisture and lack of maintenance.

Unless the rot was caused by a specific, covered event like a major storm that blew debris onto the deck and caused immediate damage, it was unlikely to be covered. My heart sank.

The conversation ended with her saying she’d have an adjuster contact me. But I already knew what was coming. The adjuster came out a week later.

He was nice, but very thorough. He examined the wood, checked the posts, and looked at the house connection. He pointed out signs of consistent moisture.

He also noted the condition of the sealant, or lack thereof.

His conclusion was clear: the rot was due to long-term exposure to moisture and insufficient maintenance. It wasn’t a sudden event. Therefore, it wasn’t covered by my policy.

It was a hard lesson. I ended up having to pay for the entire deck repair out of pocket. It cost me thousands.

That experience taught me a lot about proactive home maintenance and the real limits of insurance.

Why Does Wood Rot Happen? The Science Behind the Decay

Wood rot is essentially decay. It’s caused by specific types of fungi. These fungi eat the cellulose and lignin in wood.

These are the main building blocks that make wood strong and rigid.

For rot to set in, three things need to be present. First, you need the right kind of wood. Most common building materials like pine, fir, and spruce are susceptible.

They are great for building but can be food for rot fungi.

Second, you need a food source. This is the wood itself. The fungi break down the wood’s structure.

This makes it weak and brittle. It’s like an ongoing digestive process for the fungus.

Third, and most importantly, you need moisture and the right temperature. Fungi thrive in damp environments. Wood that stays wet for extended periods is a prime target.

Generally, wood with a moisture content of 20% or higher is at risk. Many outdoor wood structures, like decks or fences, can easily reach these levels.

Temperature also plays a role. Most rot fungi are most active in moderate temperatures. This means during spring, summer, and fall in many parts of the U.S.

Freezing temperatures can slow down or stop fungal growth, but the damage already done remains.

There are different types of rot. The most common are brown rot and white rot. Brown rot fungi attack the cellulose and hemicellulose.

This leaves behind a brittle, dark brown residue. It often cracks and shrinks. White rot fungi break down lignin as well as cellulose.

This can make the wood feel soft and spongy. It might look stringy or bleached.

Another related issue is dry rot. This term is a bit misleading. All rot needs some moisture to start.

But some fungi are very efficient at moving moisture from damper areas to drier ones. This allows them to spread even in seemingly dry wood. Dry rot fungi can cause significant damage before it’s even noticed.

The problem is that rot is a slow process. It can take months or even years to become visible. This gradual nature is why insurance companies often deny claims for rot damage.

They view it as a maintenance issue, not an insured event. It’s like a slow leak that you don’t fix. Eventually, it causes damage, but the leak itself isn’t the covered loss.

Prevention is key. Keeping wood dry is the best defense. Proper sealing, painting, and drainage are essential.

They help to keep the moisture content low. This makes it hard for rot fungi to survive and spread.

Common Causes of Wood Rot

Moisture Exposure: Constant dampness from leaks, poor drainage, or high humidity.

Poor Ventilation: Lack of air circulation traps moisture against wood surfaces.

Ground Contact: Wood touching soil absorbs moisture, leading to rot at the base.

Plumbing Leaks: Hidden leaks behind walls or under sinks can saturate wood.

Roof Leaks: Water dripping from faulty roofs can affect attic or ceiling joists.

Condensation: Warm, moist air condensing on cooler wood surfaces.

When Does Insurance Step In? Covered Perils vs. Exclusions

Your homeowners insurance policy is a contract. It spells out what is covered and what isn’t. For rot damage to be covered, it generally needs to be a direct result of a peril that your policy explicitly covers.

These are often called “named perils.”

A “named peril” is an event that is listed in your policy as being covered. Common named perils include:

- Fire and lightning

- Windstorm and hail

- Explosion

- Riot or civil commotion

- Aircraft

- Vehicles

- Smoke

- Vandalism and malicious mischief

- Theft

- Falling objects

- Weight of ice, snow, or sleet

- Accidental discharge or overflow of water or steam

- Sudden and accidental tearing apart, cracking, burning, or bulging of a steam, hot water, or air conditioning system or appliance

- Freezing

- Sudden and accidental damage from an artifical current

Now, look closely at that list. You won’t see “wood rot” directly mentioned. However, you do see “Accidental discharge or overflow of water or steam.” This is where coverage can come into play.

Let’s imagine a scenario. A pipe bursts inside a wall. Water gushes out for several hours before you discover it.

This sudden, accidental discharge of water causes significant damage. It soaks into the wooden studs and subfloor. Over the next few weeks, you start to notice a musty smell and soft spots developing in the floor.

In this case, the rotting wood damage might be covered. The insurance company would likely cover the cost to repair the water-damaged studs and subfloor. They would also cover the removal and repair of the rot itself.

This is because the rot is a direct result of the covered peril – the burst pipe.

However, the policy almost always excludes “wear and tear,” “deterioration,” “rust,” “rot,” “mold,” or “fungus” unless directly caused by a covered peril. This is the crucial distinction. If the wood rots because the roof has had a slow leak for years, or because the deck wasn’t sealed, that’s considered deterioration or wear and tear due to lack of maintenance.

That’s not covered.

Another example: A severe windstorm rips off a section of your roof. Rain pours in for a day before you can get a temporary tarp up. This rapid water intrusion causes some of your roof joists to become saturated and start to rot.

The damage from the windstorm is covered. The resulting rot damage that occurs shortly after the storm, because of that specific event, is also typically covered.

It’s vital to understand that your policy likely has limits for mold and fungus damage, even if it’s related to a covered peril. There might be sub-limits or specific conditions. Always check your policy for “mold exclusions” or “fungal remediation” clauses.

The key takeaway is this: Insurance covers sudden, accidental damage from covered events. It does not cover damage that happens gradually due to neglect or the natural aging of your home. Proving the damage stemmed from a covered event is your responsibility as the policyholder.

Rot vs. Covered Peril: A Quick Comparison

Covered Scenario

A sudden pipe burst floods your bathroom. Wood subfloor and joists rot from the prolonged water exposure. Insurance covers rot repair because it stems from a covered peril (water discharge).

Excluded Scenario

Your shower has a slow, unnoticed leak for years. The wood around it slowly rots. Insurance denies the claim because rot is due to wear and tear/lack of maintenance, not a sudden event.

The Role of Maintenance and Prevention

This is where your role as a homeowner becomes crucial. Since insurance often excludes rot damage due to neglect, preventing it is your best strategy. Think of it as a partnership with your insurance.

You take care of the routine care, and insurance steps in for the truly unexpected disasters.

Regular inspections are key. Walk around your house, inside and out. Look for signs of moisture.

Check under sinks and around toilets. Examine window frames and doors. Pay attention to areas where wood meets the ground, like decks, patios, and fences.

Decks and Patios: These are prime rot territory. Ensure they have good drainage. Water should run off, not pool.

Regularly clean them to remove debris that traps moisture. Reapply sealant or stain every 1-3 years, depending on your climate and the product used. This creates a barrier against water.

Roof and Gutters: Clogged gutters can cause water to back up against your fascia boards and soffits. This can lead to rot. Clean your gutters at least twice a year.

Check your roof for missing shingles or signs of damage after storms. Prompt repairs prevent water intrusion.

Windows and Doors: Check the seals around windows and doors. Damaged caulk or weatherstripping allows water to seep in. Look for peeling paint or soft spots on the wood.

These are early warnings.

Basements and Crawl Spaces: These areas are often damp. Ensure proper ventilation. Fix any plumbing leaks immediately.

Check for condensation on pipes or walls. A dehumidifier can be a good investment in humid climates.

Grading Around Your Home: The ground around your foundation should slope away from the house. This directs rainwater and snowmelt away. If the ground slopes towards your house, water can seep into your foundation and cause rot in sill plates or joists.

Ventilation: Good airflow helps wood dry out. Ensure attics and crawl spaces are properly ventilated. Avoid storing items directly against exterior wood siding.

This can trap moisture.

When you do find a potential issue, address it quickly. A small leak or a minor soft spot is much cheaper to fix than extensive rot damage. Early intervention can save you thousands of dollars and prevent an insurance claim denial.

Your insurance policy is a safety net for the big, unexpected events. It’s not a substitute for good home maintenance. By being proactive, you protect your investment and ensure your home remains sound and healthy for years to come.

Preventative Maintenance Checklist

- Sealant/Stain: Reapply to decks, fences, and outdoor trim every 1-3 years.

- Gutters: Clean them twice a year to prevent water backup.

- Grading: Ensure ground slopes away from your foundation.

- Caulking: Inspect and replace worn caulk around windows and doors.

- Ventilation: Check attic and crawl space vents are clear and functioning.

- Plumbing: Fix any drips or leaks under sinks and around toilets promptly.

- Exterior Walls: Look for peeling paint or soft spots on siding.

What to Do If You Discover Rotting Wood

Finding rotting wood can be stressful. But how you react can make a big difference. Here’s a step-by-step approach to handle the situation:

1. Assess the Situation (Safely):

First, try to understand the extent of the problem. Is it a small area on a deck board? Or is it structural, like a wall stud or a support beam?

Be careful if you suspect the wood is very weak. Don’t put your weight on it. You don’t want to fall through or cause further damage.

2. Identify the Likely Cause:

This is the most critical step for insurance. Try to figure out why the wood is rotting. Is there a clear, sudden cause?

- Did a storm recently damage a part of your roof or siding?

- Was there a recent plumbing leak that you fixed?

- Is it a consistent issue with poor drainage or lack of ventilation that has been ongoing?

Document everything. Take clear photos and videos of the damage and the surrounding area. Note any recent weather events or known issues.

3. Consult Your Insurance Policy:

Read your homeowners insurance policy carefully. Look for sections on water damage, mold, rot, and exclusions. Pay attention to the “named perils” and “exclusions” sections.

If you’re unsure, call your insurance agent.

4. Contact Your Insurance Company (If Applicable):

If you believe the rot is a direct result of a covered peril, contact your insurance company to file a claim. Be prepared to provide details about the suspected cause. Stick to the facts and your documentation.

Be honest. Misrepresenting the cause can lead to claim denial or policy cancellation.

5. Get Professional Opinions:

Regardless of whether you file a claim, it’s wise to get professional opinions. Contact a reputable contractor experienced in wood repair and rot remediation. They can assess the damage and provide an estimate for repairs.

If you are filing a claim, consider hiring an independent public adjuster. They work for you, not the insurance company. They can help assess the damage accurately and negotiate with the insurer.

6. Focus on Repair and Prevention:

Once you have a plan, focus on getting the repairs done correctly. Ensure the contractor addresses the root cause of the rot, not just the damaged wood. This might involve fixing a leaky pipe, improving drainage, or adding ventilation.

Implement preventative maintenance to stop future rot from forming. This includes sealing wood, cleaning gutters, and ensuring proper airflow.

Remember, insurance is meant to cover sudden, accidental damage. Proving that your rotting wood issue stems from such an event is key to getting coverage. If it’s a result of long-term wear and tear or lack of maintenance, you’ll likely be responsible for the repair costs.

Quick Action Steps for Rot Discovery

Immediate: Take photos and notes of the damage and surroundings.

Investigate: Try to determine the root cause (sudden event vs. slow decay).

Review: Check your insurance policy for relevant coverage and exclusions.

Contact: Inform your insurance company if you suspect a covered peril caused the rot.

Professionals: Get estimates from qualified contractors and possibly an independent adjuster.

Repair: Address the cause and fix the damaged wood thoroughly.

Prevent: Implement regular maintenance to avoid future issues.

When Is Rot NOT Covered? Common Exclusion Scenarios

As we’ve discussed, insurance policies have specific exclusions. These are common reasons why a claim for rotting wood might be denied. Understanding these can help you manage your expectations and focus on preventative measures.

1. Gradual Deterioration/Wear and Tear:

This is the most common reason for denial. If the wood has been slowly rotting over months or years due to constant moisture, lack of sealing, or exposure to the elements, it falls under wear and tear. Insurance covers unexpected events, not the natural aging and decay of your home.

2. Lack of Maintenance:

This is closely related to wear and tear. If your home has not been properly maintained – for example, if a deck has not been sealed, gutters have been consistently clogged, or a minor leak was ignored – the resulting rot will likely be excluded. The insurance company views this as a failure to mitigate potential damage.

3. Mold, Fungus, and Rot Exclusions:

Many policies contain specific clauses that exclude damage from mold, fungus, and rot. While they might make an exception if these are caused by a covered peril, the baseline is often exclusion. This means if the rot is the primary problem and not a secondary effect of a sudden event, it’s usually not covered.

4. Infestation:

Damage caused by insects like termites or carpenter ants can lead to wood weakening. However, the rot itself is usually a separate issue. While some policies might cover insect damage (often with limitations), they typically won’t cover the secondary rot that results from it unless it’s tied to a covered peril.

5. Flood Damage (Standard Policies):

Standard homeowners insurance policies do not cover flood damage. If your home is in a flood-prone area and prolonged water exposure leads to wood rot, you would need separate flood insurance to cover such damage. Flood insurance policies also have specific terms regarding how damage is covered.

6. Foundation Issues:

Sometimes, foundation problems can lead to moisture issues that cause rot. Most policies exclude damage related to the settling, shrinking, or expanding of the foundation. If rot is a secondary effect of these excluded issues, it’s unlikely to be covered.

7. Contractor Negligence (Sometimes):

In some cases, if rot is caused by faulty workmanship during a previous renovation, the situation can become complex. Your recourse might be against the contractor, not your insurer, unless the faulty work itself caused a sudden, accidental event. This often requires legal consultation.

It’s important to remember that insurance policies can vary. The exact wording of exclusions is critical. Always refer to your specific policy documents and discuss any concerns with your insurance agent or a legal professional specializing in insurance law if needed.

Common Rot Claim Denials

Reason for Denial

Slowly developing rot from years of moisture exposure.

Policy Term

Wear and Tear / Deterioration

Reason for Denial

Rot due to unsealed deck that hasn’t been maintained.

Policy Term

Lack of Maintenance / Neglect

Reason for Denial

Mold and fungus growth found without a linked covered peril.

Policy Term

Mold / Fungus / Rot Exclusion

When to Call a Professional and What to Expect

Deciding when to call a professional for wood rot is usually straightforward: as soon as you suspect it. The sooner you act, the less damage there is, and the less it will cost to fix.

Who to Call:

- General Contractor: For most visible rot issues on decks, fences, or exterior trim. They can assess the damage and perform repairs.

- Plumber: If you suspect rot is caused by a leaking pipe inside a wall or under a sink.

- Roofer: If you think a roof leak is contributing to rot in the attic, soffits, or fascia.

- Structural Engineer: If you suspect rot has compromised the structural integrity of your home (e.g., in major beams, joists, or foundation elements).

- Restoration Company: These companies specialize in dealing with water damage, mold, and rot. They often have the expertise and equipment to handle complex situations.

- Independent Public Adjuster: If you are filing an insurance claim and want an expert advocate to assess the damage and negotiate with your insurer.

What to Expect:

When a professional visits, they will typically:

- Inspect the Area: They’ll look at the visible signs of rot. They might use tools like a moisture meter or a probing tool to check the extent of the decay.

- Identify the Cause: A good professional will not just fix the rot; they will try to find out why it happened. This might involve checking for leaks, poor drainage, or ventilation issues.

- Determine the Scope: They will figure out how much wood needs to be replaced and if any structural elements are affected.

- Provide an Estimate: You will receive a detailed quote for the repair work. This should include labor, materials, and disposal of damaged items.

- Explain the Repair Process: They should walk you through the steps they will take to fix the problem and prevent recurrence.

If you’re dealing with a potential insurance claim, the contractor or restoration company can often help you with the documentation needed for the claim. They can provide detailed reports and repair estimates that your insurance company will require.

Don’t hesitate to get multiple quotes if the repair is significant. Ask for references and check reviews for any contractor you consider hiring. Ensure they are licensed and insured in your state.

Frequently Asked Questions About Rotting Wood and Insurance

Will my insurance pay to replace my entire deck if part of it has rot?

Generally, no. Insurance typically covers the cost to repair or replace only the damaged portion of the deck that was affected by a covered peril. If the rot is due to wear and tear, only the rotted sections would be considered, and likely denied.

Replacement of the entire structure is usually not covered unless the damage is widespread and directly caused by a covered event.

What is the difference between rot and mold when it comes to insurance coverage?

Both mold and rot are often excluded from standard homeowners insurance policies unless they are a direct result of a covered peril like a sudden pipe burst or storm damage. Many policies have specific clauses excluding mold, fungus, and rot damage. If mold or rot appears gradually due to moisture issues or lack of maintenance, it’s unlikely to be covered.

How long does an insurance company usually take to investigate a rot claim?

The timeline can vary. Once a claim is filed, an adjuster will typically be assigned within a few days. The inspection and assessment process can take anywhere from a few days to a couple of weeks, depending on the complexity of the damage and the adjuster’s workload.

Prompt communication and providing all requested documentation can speed up the process.

Can I get my insurance to pay for preventative maintenance like sealing my deck?

No, homeowners insurance does not cover routine preventative maintenance. Its purpose is to protect against sudden and accidental loss. Tasks like sealing decks, cleaning gutters, or painting are considered the homeowner’s responsibility for maintaining the property and preventing future issues.

What if the rot is in my sill plate or foundation?

Rot in these critical structural areas can be serious. If the rot is directly caused by a covered peril (e.g., a sudden flood or a specific pipe burst that saturated the area), the resulting damage, including the rot, might be covered. However, if it’s due to long-term moisture issues, poor drainage around the foundation, or general deterioration, it will likely be excluded.

Should I try to fix minor rot myself before calling an insurance company?

It’s generally advisable to contact your insurance company first if you believe the damage might be covered. Making repairs before an adjuster has assessed the situation could jeopardize your claim. If the damage is minor and clearly due to wear and tear, you might choose to fix it yourself to avoid a claim that would likely be denied anyway.

However, for anything potentially covered, let the insurer inspect first.

Final Thoughts on Rot and Your Home Protection

Dealing with wood rot in your home can be a frustrating and expensive problem. Understanding how your homeowners insurance policy works is your first line of defense. Remember, insurance is primarily for sudden, accidental events.

Gradual decay, wear and tear, and damage from lack of maintenance are typically not covered.

The key to potential coverage lies in proving the rot is a direct result of a covered peril. Always document the damage and try to identify the root cause. Be honest with your insurance company.

Proactive maintenance is your best friend. It prevents rot from starting and saves you money and headaches in the long run. Protect your home by staying vigilant and addressing moisture issues immediately.